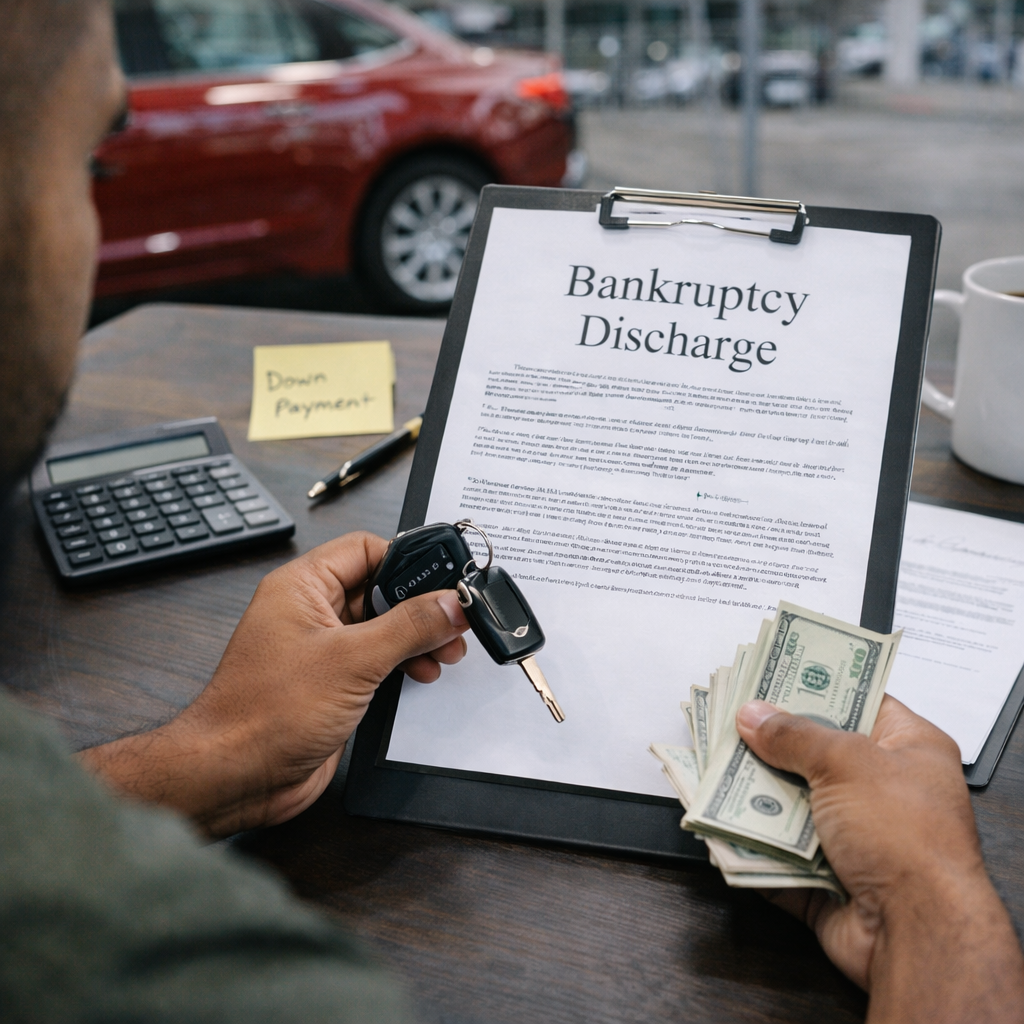

How to Buy a Used Car in Brooklyn After Bankruptcy

Let’s get something straight:

A recent bankruptcy does not mean you’re locked out of buying a car.

It does mean lenders will look at you differently. And that’s not personal — it’s risk assessment. The good news? With the right timing, documentation, and structure, approval is absolutely achievable.

The key is discipline and positioning.

Wait for the Right Timing

Timing matters more than most people realize.

- After a bankruptcy discharge, many lenders will consider you.

- During Chapter 13, some lenders may approve you with trustee authorization.

- The longer you’ve shown financial stability after filing, the stronger your case becomes.

If you rush immediately without preparation, you’ll limit your options and likely face higher rates.

Patience here pays off.

Rebuild and Stabilize First

Before applying, tighten up your financial profile.

Lenders want to see:

- No new late payments

- Bills paid consistently

- Stable employment

- Reliable income documented through pay stubs or bank statements

Your recent behavior matters more than the bankruptcy itself. If you demonstrate control and consistency, lenders notice.

Bring a Meaningful Down Payment

This is where strategy comes in.

A 10%–20% down payment can:

- Offset perceived risk

- Improve approval odds

- Reduce your loan-to-value ratio

- Potentially lower your interest rate

After bankruptcy, lenders want to see commitment. A solid down payment shows skin in the game.

Choose Practical, Reliable Vehicles

This is not the moment to overreach.

Focus on:

-

Reliable used vehicles

-

Moderate price points

-

Affordable monthly payments

Stretching for a high-priced car right after bankruptcy puts you back in a vulnerable position. The goal right now isn’t status — it’s rebuilding credit strength.

Keep it practical. Upgrade later.

Check Insurance Before Finalizing

Many buyers forget this step.

After bankruptcy, insurance premiums can sometimes be higher depending on your profile. Before signing:

- Get an insurance quote

- Calculate total monthly cost (car payment + insurance)

- Make sure it fits comfortably in your budget

If the numbers feel tight, they are tight.

Yes, Approval Is Possible

We regularly work with buyers in Brooklyn navigating car purchases after bankruptcy. The focus isn’t just on getting you approved — it’s on matching you with lenders who understand your situation and structuring a deal that supports your financial recovery.

Bankruptcy is a reset — not a life sentence.

If you approach this strategically, your next car can be part of your rebuild — not another setback.